Receiving an inheritance can be one of life's most emotionally complex financial events. On one hand, it may provide financial opportunities you never expected. On the other, it often comes during a period of grief, uncertainty, and significant life change.

While it may be tempting to immediately invest the money, pay off debt, or make major purchases, the best first step is often much simpler: pause. Giving yourself time to process both the emotional and financial implications can help you make thoughtful decisions that align with your long-term goals.

An inheritance can create opportunities, but it also comes with important decisions. The goal isn't to make decisions quickly—it's to make the right decisions. By taking a thoughtful approach, you can make choices that not only protect your financial future but also honor the legacy of the person who left you this gift.

Quick Answer

If you've recently received an inheritance, your first priority shouldn't be deciding how to invest the money. Instead, focus on understanding what you've inherited, giving yourself time to make informed decisions, and building a plan before making major financial moves.

For most people, the first steps include:

- Pause before making significant financial decisions.

- Identify every asset you've inherited.

- Understand the tax implications.

- Determine how the inheritance fits into your financial goals.

- Create a long-term plan before investing or spending.

Every inheritance is unique. Taking a thoughtful approach can help you avoid costly mistakes and make decisions that support your long-term financial future.

Why This Matters

An inheritance can affect nearly every area of your financial life. Depending on what you've inherited, it may influence your retirement timeline, investment strategy, tax situation, estate planning decisions, insurance needs, debt repayment priorities, charitable giving goals, and even how you think about your family's financial future.

That's why it's helpful to think of an inheritance not as a windfall, but as an opportunity to step back and evaluate your overall financial plan. The decisions you make today can have an impact for years—or even decades—to come.

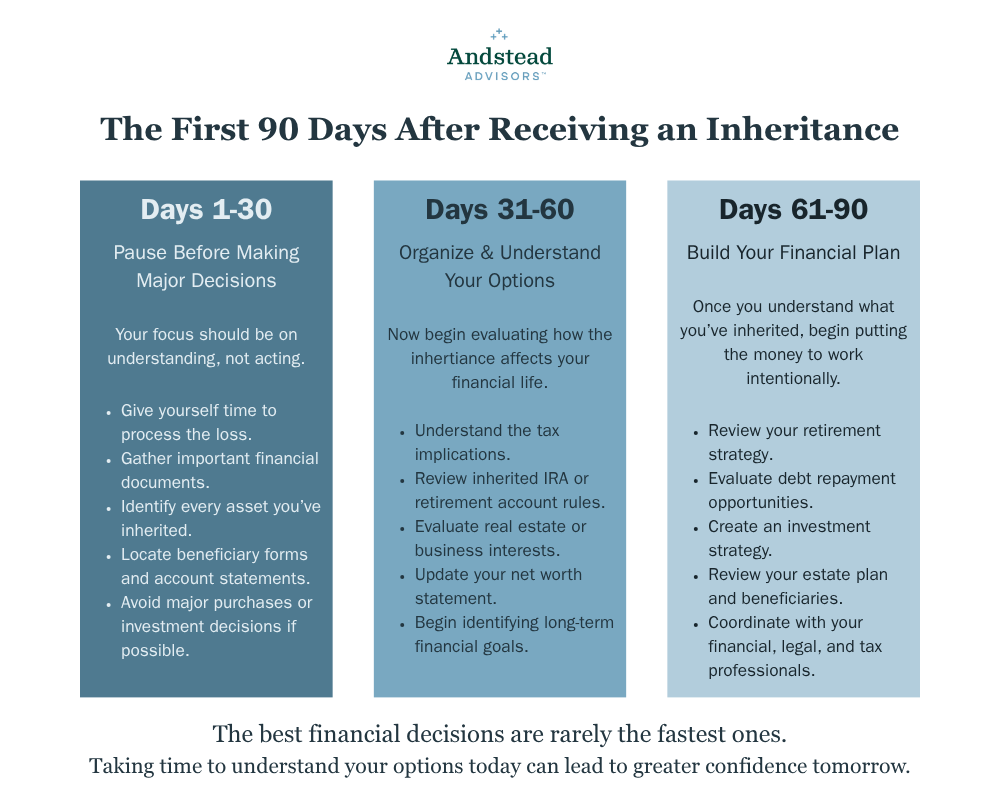

Your First 30 Days

The first few weeks after receiving an inheritance are rarely the right time to make major financial decisions. If possible, resist the urge to make large purchases, immediately invest the money, pay off every debt, give significant gifts, or make dramatic lifestyle changes.

Instead, focus on understanding exactly what you've inherited and gathering the information you'll need to make informed decisions. Taking time to create a plan often leads to better long-term outcomes than reacting emotionally.

Understand What You've Actually Inherited

Not all inherited assets are treated the same. Understanding what you've inherited is one of the most important first steps because different assets come with different tax rules, distribution requirements, and planning considerations.

You may inherit:

- Cash

- Brokerage accounts

- Traditional IRAs

- Roth IRAs

- 401(k) accounts

- Real estate

- A business interest

- Life insurance proceeds

- Trust assets

Each asset may require a different strategy.

Inheritance Planning at a Glance

| Asset | Tax Considerations | Planning Considerations |

|---|---|---|

| Cash | Generally not taxable as income | Emergency fund, debt reduction, investing |

| Brokerage Account | May receive a step-up in cost basis | Investment strategy and future capital gains |

| Traditional IRA | Distribution rules and income taxes may apply | Withdrawal timing and tax planning |

| Roth IRA | Distribution rules still apply | Long-term tax-free growth potential |

| Real Estate | May receive a step-up in basis | Keep, sell, or rent the property |

| Business Interest | Valuation and ownership considerations | Succession planning and long-term goals |

Your First Priority Depends on What You Inherited

| If You Inherited... | Your First Priority |

|---|---|

| Cash | Decide how it fits into your financial plan before spending or investing. |

| Brokerage Account | Review the cost basis and your investment strategy. |

| Traditional IRA | Understand distribution rules and potential tax implications. |

| Roth IRA | Review distribution requirements and long-term planning opportunities. |

| Real Estate | Determine whether keeping, selling, or renting aligns with your goals. |

| Business Interest | Evaluate ownership, valuation, and succession considerations. |

Simply knowing what you've inherited can significantly influence the decisions you make next.

Your Next 90 Days

Once you've had time to process the inheritance, begin evaluating how it fits into your overall financial picture. This is often the right time to organize documents, understand tax implications, and begin developing a long-term financial plan.

Understand the Tax Implications

One of the biggest misconceptions about inheritances is that everything is tax-free. While inherited assets generally aren't considered taxable income, different assets follow different tax rules.

For example:

- Appreciated investments and real estate may receive a step-up in cost basis.

- Inherited retirement accounts often have distribution requirements.

- Future withdrawals from certain inherited retirement accounts may be taxable.

- Some states have inheritance or estate taxes.

Some questions worth asking include:

- Does this asset receive a step-up in cost basis?

- Are there required distributions?

- Will future withdrawals be taxable?

- Are there state inheritance or estate tax considerations?

- How could this affect my overall tax situation?

Understanding these rules before making financial decisions can help prevent costly surprises.

Decide What You Want This Inheritance to Accomplish

Rather than asking, "What should I do with this money?", consider asking, "What do I want this inheritance to do for me?"

Perhaps it could help strengthen your emergency savings, eliminate high-interest debt, improve your retirement readiness, purchase a home, fund a child's education, support charitable causes, preserve a family legacy, or simply create greater financial flexibility.

Every inheritance has a purpose. The goal is identifying yours before making financial decisions.

Questions to Ask Yourself Before Making Any Decisions

Before deciding what to do with your inheritance, take a moment to reflect on your broader financial picture.

Ask yourself:

- Do I need this money immediately?

- What financial goals could this inheritance help me achieve?

- Am I carrying high-interest debt?

- Would strengthening my emergency fund improve my financial security?

- How does this affect my retirement goals?

- Have I considered the tax implications?

- Would the person who left me this inheritance have wanted it used in a particular way?

There may not be one universally correct answer. Taking time to think through these questions often provides clarity and helps you make more confident decisions.

Common Mistakes to Avoid

Spending Too Quickly

An inheritance can feel like unexpected money, but it's often the result of someone else's lifetime of saving and planning. Giving yourself time before making large purchases helps ensure your decisions support your long-term goals rather than short-term emotions.

Making Financial Decisions While Grieving

Grief affects judgment. Whenever possible, avoid making major financial commitments immediately after losing a loved one unless circumstances require immediate action.

Ignoring Tax Considerations

Different inherited assets follow different tax rules. Understanding those rules before selling investments or taking distributions can help prevent unexpected tax consequences.

Investing Before Creating a Plan

Investments should support your financial goals—not determine them. A thoughtful financial plan almost always comes before a successful investment strategy.

Treating Every Asset the Same

Cash, inherited retirement accounts, brokerage accounts, real estate, and business interests all require different planning approaches. A strategy that makes sense for one asset may not be appropriate for another.

When You May Need to Act More Quickly

While slowing down is often the right approach, there are situations where waiting too long may create additional challenges. Depending on what you've inherited, you may need to address required deadlines for inherited retirement accounts, estate administration responsibilities, ongoing expenses related to inherited real estate, business ownership decisions, or immediate cash flow needs of the estate.

If you're unsure whether time-sensitive decisions apply to your situation, identifying those deadlines early can help you make informed choices without unnecessary pressure.

Long-Term Planning

Once you've organized the inheritance and understand the tax implications, it's time to determine how it fits into your long-term financial plan. That may include reviewing your retirement goals, investment strategy, debt repayment priorities, insurance coverage, estate planning documents, beneficiary designations, and charitable giving plans.

An inheritance isn't simply a financial event. For many people, it becomes an opportunity to revisit their entire financial plan and ensure it reflects both their current circumstances and future goals.

What We've Learned Helping Clients

One thing we've noticed over the years is that people often feel pressure to "do something" with an inheritance immediately. In our experience, the families who make the most confident decisions are usually the ones who give themselves permission to slow down first.

Taking time to understand the assets you've inherited, evaluate the tax implications, and determine how the inheritance fits into your broader financial picture often leads to better long-term outcomes than reacting quickly. We've also found that inheritances naturally encourage people to reflect on what matters most—not just financially, but personally.

An inheritance isn't simply about managing money. It's about making thoughtful decisions that honor both your loved one's legacy and your own future.

Final Thoughts

Receiving an inheritance can change your financial life, but it doesn't require you to have all the answers immediately. The most successful financial decisions are rarely the fastest ones.

By taking time to understand what you've inherited, evaluating the tax implications, and building a thoughtful financial plan, you can make decisions with greater confidence and purpose.

Rather than asking, "What should I do with this money?", consider asking, "How can this inheritance best support the life I want to build—and the legacy I want to continue?" That shift in perspective often leads to decisions you'll feel good about for years to come.

Frequently Asked Questions

Q: What should I do first after receiving an inheritance?

A: The first step is to slow down. Before making major financial decisions, take time to understand what you've inherited, organize important documents, and identify any tax or legal considerations. In many cases, building a plan before investing or spending can lead to better long-term outcomes.

Q: Should I invest my inheritance immediately?

A: Not necessarily. While every situation is different, many people benefit from taking time to evaluate their financial goals, understand the assets they've inherited, and consider any tax implications before making investment decisions.

Q: Is an inheritance considered taxable income?

A: In most cases, an inheritance itself is not considered taxable income. However, certain inherited assets—such as traditional retirement accounts—or future investment earnings may have tax implications.

Q: What is a step-up in cost basis?

A: A step-up in cost basis generally adjusts the value of inherited investments or real estate to their fair market value at the original owner's death. This can reduce future capital gains taxes if the asset is later sold.

Q: What happens if I inherit an IRA?

A: Inherited IRAs have specific distribution rules that depend on your relationship to the original owner and current tax laws. Some beneficiaries must withdraw the assets within a certain timeframe, while others may have different options available.

Q: Should I pay off debt with my inheritance?

A: It depends. Paying off high-interest debt may be a smart financial decision for some people, but it should be evaluated alongside other goals such as retirement planning, emergency savings, and investment opportunities.

Q: What if I inherit a house?

A: If you inherit real estate, you'll need to decide whether keeping, selling, or renting the property best aligns with your financial goals. It's also important to understand any maintenance costs, taxes, and potential capital gains considerations.

Q: What if I inherit a family business?

A: Inheriting a business often involves additional considerations, including ownership structure, valuation, succession planning, tax implications, and long-term management decisions.

Q: How long should I wait before making financial decisions?

A: There's no universal timeline, but unless immediate deadlines apply, many financial professionals recommend avoiding major financial decisions until you've had time to understand the inheritance, process the emotional impact, and develop a thoughtful plan.

Q: Can receiving an inheritance affect my financial plan?

A: Yes. An inheritance may influence your retirement timeline, investment strategy, debt repayment priorities, estate plan, insurance needs, and other long-term financial goals. It's often a good opportunity to review your overall financial plan.

Q: Should I hire a financial advisor after receiving an inheritance?

A: Depending on the size and complexity of the inheritance, professional guidance may help you understand tax considerations, evaluate investment options, coordinate with other professionals, and develop a long-term financial plan that aligns with your goals.

Q: What are the biggest mistakes people make after receiving an inheritance?

A: Some of the most common mistakes include making emotional financial decisions, spending too quickly, overlooking tax implications, investing without a plan, and treating every inherited asset the same when different assets may require different strategies.

About Andstead Advisors

Andstead Advisors is an independent financial planning and wealth management firm headquartered in Denver's Denver Tech Center, serving individuals, families, retirees, and business owners throughout Colorado and across the country. Our team provides comprehensive financial planning, investment management, retirement planning, business owner solutions, retirement plan consulting, business succession planning, cash balance plan strategies, profit sharing plans, and Solo 401(k) guidance. As fiduciary advisors, we help clients make informed financial decisions through personalized advice, long-term planning, and ongoing partnership designed to support their financial goals at every stage of life.