One of the first questions many people ask when considering professional financial advice is, "How much does a financial advisor cost?" The answer depends on how the advisor is compensated and the services they provide. Some advisors charge a percentage of the assets they manage, while others charge flat planning fees, hourly rates, commissions, or a combination of these methods.

While cost is certainly important, it's only part of the equation. Understanding what's included in those fees is often even more valuable. The lowest-cost advisor isn't always the best value, just as the highest-cost advisor isn't always the best fit. By understanding how financial advisors charge—and what you're receiving in return—you'll be in a much better position to compare firms and choose an advisory relationship that aligns with your needs.

The Four Most Common Ways Financial Advisors Charge

Most financial advisors use one of four primary fee structures. Each has its own advantages and tradeoffs, and understanding how they work can help you compare advisors more confidently.

Assets Under Management (AUM)

An Assets Under Management (AUM) fee is one of the most common pricing models for ongoing investment management. Rather than paying a flat dollar amount, you pay a percentage of the assets your advisor manages on your behalf.

For example, if you have a $500,000 portfolio and your advisor charges 1.00% annually, your annual advisory fee would be approximately $5,000. An AUM fee often includes ongoing portfolio management, regular review meetings, investment monitoring, and other planning services, although what's included varies from firm to firm. That's why it's important to ask exactly what services are covered before comparing fees.

Advantages

- Ongoing relationship

- Fee grows only as your portfolio grows

- Often includes continuous planning and investment management

Potential Drawbacks

- Fees increase as your assets increase

- Services included can vary significantly between firms

Flat Fee Financial Planning

Some advisors charge a fixed fee for creating a financial plan or providing ongoing planning services. Depending on the scope of work, the fee may cover a one-time engagement or an ongoing advisory relationship. This pricing structure offers predictable costs and is often well suited for individuals seeking comprehensive financial planning without ongoing investment management.

Advantages

- Predictable pricing

- Not directly tied to portfolio size

- Often appropriate for clients seeking planning without investment management

Hourly Financial Planning

Some advisors bill by the hour for consultations or specific financial questions. This approach can work well for individuals who need guidance on a particular topic rather than an ongoing advisory relationship.

Advantages

- Pay only for the advice you need

- Good for targeted planning questions

Potential Drawbacks

- Ongoing planning generally requires additional meetings and additional fees

Commission-Based Compensation

Some advisors receive commissions from the sale of certain financial products. Rather than paying the advisor directly, compensation comes from the product provider. Whenever commissions are involved, it's important to understand how your advisor is compensated, whether they act as a fiduciary, and whether alternative recommendations may also be appropriate.

What Does "1%" Actually Mean?

Many people hear that a financial advisor charges "about 1%" and assume it isn't significant. After all, one percent sounds relatively small.

But percentages can be deceiving. As your portfolio grows, even what appears to be a modest advisory fee represents a meaningful dollar amount. Looking at advisory fees in dollars—not just percentages—makes it much easier to understand the actual cost and compare firms.

| Portfolio Value | 1% Annual Fee |

|---|---|

| $250,000 | $2,500 |

| $500,000 | $5,000 |

| $750,000 | $7,500 |

| $1,000,000 | $10,000 |

| $2,000,000 | $20,000 |

Understanding the dollar amount helps put advisory fees into perspective and makes it easier to compare firms and services.

Understanding Tiered Advisory Fees

Many financial advisory firms—including Andstead Advisors—use a tiered fee schedule rather than charging one flat percentage across an entire portfolio.

With tiered pricing, different portions of your portfolio are billed at different rates. One of the biggest misconceptions is that once your account reaches a new tier, your entire portfolio is charged at the lower percentage. That's generally not how tiered pricing works.

Instead, each tier is calculated independently, much like the way progressive income tax brackets work. Only the assets that fall within each tier are billed at that tier's corresponding rate, and those amounts are then added together to determine the total advisory fee.

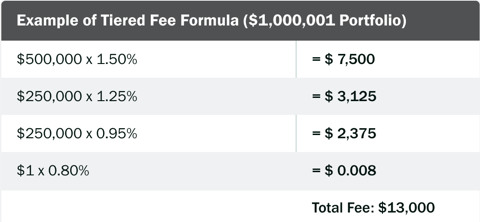

Tiered Fee Formula Example

As this example illustrates, each tier is calculated independently and then added together to determine the total annual advisory fee.

How Andstead Advisors Charges for Investment Management

At Andstead Advisors, we believe in being transparent about how investment management fees are calculated. Our investment management fee schedule is tiered, meaning that as assets under management increase, the fee applied to additional assets decreases.

Rather than charging one percentage across an entire portfolio, each asset tier is billed independently according to our published fee schedule. This approach allows larger portfolios to benefit from progressively lower marginal fee rates while maintaining a consistent and transparent pricing structure.

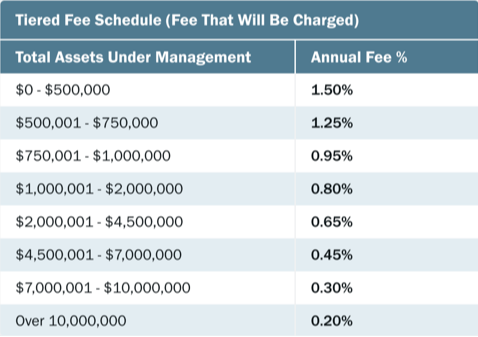

Andstead Advisors Tiered Fee Schedule

Rather than charging a single percentage across an entire portfolio, each asset tier is billed according to the schedule above.

This approach allows larger portfolios to benefit from progressively lower marginal fee rates while maintaining a consistent and transparent pricing structure.

What's Included in an Advisory Fee?

When people think about hiring a financial advisor, they often picture someone selecting investments or managing a portfolio. In reality, investment management is frequently just one part of the relationship.

Depending on the firm, an advisory relationship may also include:

- Comprehensive financial planning

- Retirement planning

- Investment management

- Tax planning opportunities

- Estate planning coordination

- Insurance reviews

- Cash flow planning

- Business owner planning

- Ongoing portfolio monitoring

- Regular review meetings

- Behavioral coaching during market volatility

Because services vary from firm to firm, it's important to understand exactly what's included before comparing fees.

The Cheapest Advisor Isn't Always the Best Value

When comparing financial advisors, it's natural to focus on cost first. But fees tell only part of the story.

A better question is:

What am I actually receiving for the fee I'm paying?

Consider the difference between these two advisors:

Advisor A

- Lower fee

- Investment management only

Advisor B

- Higher fee

- Investment management

- Retirement planning

- Tax planning guidance

- Estate planning coordination

- Insurance reviews

- Ongoing financial planning

Which advisor provides better value?

The answer depends on your needs and the services you're actually receiving. Looking only at the percentage you pay may overlook the broader value comprehensive financial planning can provide over many years.

Questions to Ask About Advisor Fees

Before hiring a financial advisor, consider asking:

- How are you compensated?

- What services are included in the fee?

- Are financial planning services included?

- Are there any additional planning or consulting fees?

- Are there account minimums or minimum annual fees?

- Are investment expenses separate from advisory fees?

- How often are advisory fees billed?

Understanding these answers makes it much easier to compare advisors on more than price alone.

What We've Learned Helping Clients

One thing we've noticed over the years is that many people assume they're paying an advisor simply to manage investments.

In reality, some of the most valuable conversations happen when markets aren't moving at all. Helping clients make confident retirement decisions, identify tax planning opportunities, coordinate estate planning, navigate business transitions, or simply avoid emotional investing during periods of market volatility often creates value that's difficult to measure on a quarterly statement—but incredibly meaningful over the long term.

That's why we encourage people to evaluate advisory relationships based not only on cost, but on the breadth of guidance, planning, and partnership they receive throughout the relationship.

Final Thoughts

Financial advisor fees vary depending on the advisor, the services offered, and how those services are delivered.

While it's important to understand how much an advisor charges, it's just as important to understand what those fees include. A lower fee doesn't automatically mean better value, just as a higher fee doesn't necessarily mean you're paying too much.

The right question isn't simply, "How much does a financial advisor cost?" It's "What value am I receiving for that cost?"

When you understand how advisors are compensated, what services are included, and how those fees are calculated, you'll be in a much stronger position to choose an advisory relationship that supports your long-term financial goals.

Frequently Asked Questions

Q: How much does a financial advisor cost?

A: Financial advisor costs vary depending on how the advisor is compensated. Common fee structures include assets under management (AUM), flat planning fees, hourly fees, commissions, or a combination of these methods.

Q: What is the average financial advisor fee?

A: Many investment advisors who charge an Assets Under Management (AUM) fee charge around 1% annually, though fees vary based on account size, services provided, and the firm's pricing structure. Some firms use tiered fee schedules where the percentage decreases as assets increase.

Q: What is an Assets Under Management (AUM) fee?

A: An AUM fee is an annual fee calculated as a percentage of the assets your advisor manages. Rather than paying a flat dollar amount, the fee is based on the value of your investment portfolio.

Q: What is a tiered advisory fee schedule?

A: A tiered fee schedule applies different fee percentages to different portions of your portfolio. As assets increase, the fee on additional assets typically decreases, rather than applying one rate to the entire portfolio.

Q: Are financial advisor fees tax deductible?

A: Tax laws change over time, and whether advisory fees are deductible depends on your specific situation and applicable tax rules. It's best to consult your tax professional regarding your circumstances.

Q: Do financial advisors charge separately for financial planning?

A: It depends on the firm. Some advisors include comprehensive financial planning as part of their advisory fee, while others charge a separate planning fee or offer planning as a standalone service.

Q: What services are typically included in an advisory fee?

A: Depending on the advisor, an advisory fee may include investment management, retirement planning, tax planning guidance, estate planning coordination, insurance reviews, cash flow planning, and ongoing financial advice. Always ask what services are included before hiring an advisor.

Q: Is a lower financial advisor fee always better?

A: Not necessarily. A lower fee may also mean fewer services. When comparing advisors, consider both the cost and the value provided, including the scope of planning, ongoing support, and expertise.

Q: How often are financial advisor fees charged?

A: Many advisors bill advisory fees quarterly, although billing schedules vary by firm. Ask your advisor how and when fees are calculated and deducted.

Q: Are investment expenses included in an advisory fee?

A: Not always. Investment expenses, such as mutual fund or ETF operating expenses, are often separate from the advisory fee. Ask your advisor to explain all costs associated with your investments.

Q: What questions should I ask about a financial advisor's fees?

A: Ask how the advisor is compensated, what services are included, whether there are additional planning or consulting fees, how often fees are billed, and whether there are any account minimums or other investment-related expenses.

Q: How do I know if a financial advisor is worth the cost?

A: Rather than focusing solely on the fee percentage, evaluate the overall value of the relationship. Consider the advisor's experience, planning process, ongoing guidance, accessibility, and the services provided beyond investment management.

About Andstead Advisors

Andstead Advisors is an independent financial planning and wealth management firm headquartered in Denver's Denver Tech Center, serving individuals, families, retirees, and business owners throughout Colorado and across the country. Our team provides comprehensive financial planning, investment management, retirement planning, business owner solutions, retirement plan consulting, business succession planning, cash balance plan strategies, profit sharing plans, and Solo 401(k) guidance. As fiduciary advisors, we help clients make informed financial decisions through personalized advice, long-term planning, and ongoing partnership designed to support their financial goals at every stage of life.